New findings from Addition Wealth show how rising costs and economic volatility affected employees across income levels.

Key Survey Findings at a Glance

58% of employees report moderate to high stress, including half of those who say they are in a strong financial position

71% of employees would feel moderate to high stress if their paycheck were delayed by just one week

57% of employees report health effects from financial stress, and among those highly stressed, 86% experience at least one health impact¹

In many ways, 2025 was expected to be a year of financial stabilization. Inflation cooled from 2022 peaks and many households continued saving and planning for the future. Yet for many individuals, financial stress didn’t ease this year, it intensified.

Rising everyday costs, new tariffs affecting the price of goods, and continued economic uncertainty reshaped how people experienced their finances this year. Trade policy changes increased costs across supply chains, showing up in the prices of everyday essentials. We saw some highly visible price spikes, such as the cost of eggs and coffee reaching record highs.

Against this backdrop, Addition Wealth conducted its 2025 Employee Survey to better understand how employees were navigating their finances. The findings reveal an important shift: financial stress in 2025 was less about income or savings alone, and more about uncertainty, confidence, and the ability to manage change. Across industries, roles, and income levels, people are doing many of the “right” things financially, yet stress persists.

People are saving, planning, and staying engaged

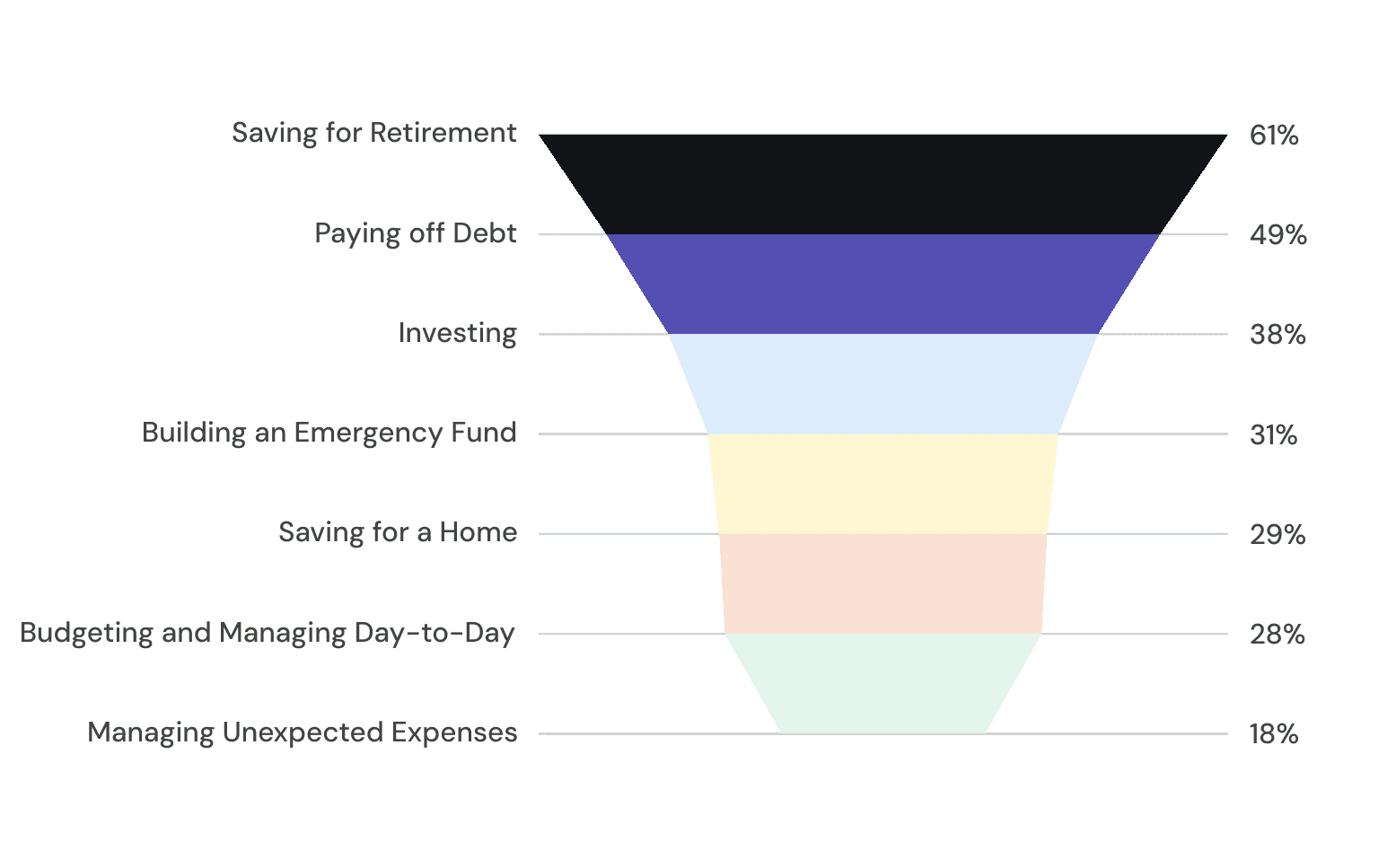

Across respondents, most people are taking consistent steps to manage their finances, even amid uncertainty. Saving for retirement also emerged as the top goal overall, with 61% listing it as a priority.²

Respondents identified a range of financial goals for the year, reflecting both long-term planning and day-to-day financial needs.³

61% are saving for retirement

49% are paying off debt

38% are investing

31% are building an emergency fund

29% are saving for a home

28% are budgeting and managing day-to-day spending

18% are managing unexpected expenses

Taken together, these goals show a workforce that is actively trying to build stability in a year marked by uncertainty. People are saving, planning, and prioritizing what they can control, even as broader economic conditions continue to shape how confident they feel day to day.

Stress Persists Even When Finances Are Strong, Impacts Health, Relationships, and Work

More than half of survey respondents (58%) reported moderate to high financial stress and that stress does not disappear with stronger financial health. Even among individuals who rated their finances as strong, 50% still reported moderate to high stress, and 31% experienced health impacts related to financial pressure.⁴

These findings point to an important shift. Financial wellbeing today is no longer defined solely by income, savings, or benefits. It is increasingly shaped by confidence, clarity, and the ability to manage ongoing change. Without guidance and structure, even financially stable individuals can feel overwhelmed by money.

The effects of financial stress extend well beyond finances. Across respondents:

57% reported health impacts, most commonly affecting mental health (49%) and sleep (39%)

29% said financial stress strained their relationships

37% reported difficulty focusing at work⁵

Among individuals experiencing high financial stress, the impact is even more pronounced: 86% reported at least one health-related effect, underscoring how deeply financial pressure influences overall wellbeing and daily functioning.

Younger Generations Are Engaged and Under Pressure

Millennials and Gen Z reported the highest levels of financial stress, with 88% experiencing moderate to high stress. At the same time, they are highly engaged:

93% think about their finances daily or weekly

Retirement savings, emergency funds, and debt repayment are top priorities⁶

Our survey found that 76% of employees have debt, yet only 39% actively follow a debt plan, compared to 48% of Baby Boomers.⁷ This combination of high awareness and low follow-through suggests that engagement alone isn’t enough. Without clear frameworks and guidance, constant attention to finances can increase stress rather than reduce it.

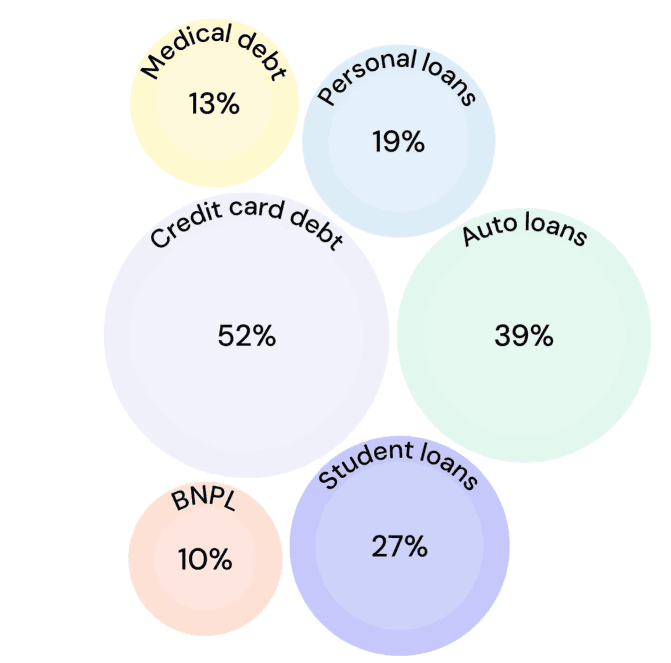

The Mix of Debt Is Changing, Adding New Layers to Financial Stress

Debt continues to be a reality for many households, but the types of debt people carry in 2025 show how financial pressures have evolved. More than half of respondents (52%) hold credit card debt, and many also manage auto loans (39%), student loans (27%), personal loans (19%), or medical debt (13%).

A notable shift is the growing presence of short-term installment debt. Ten percent of respondents report Buy Now, Pay Later (BNPL) balances, reflecting how these tools have become part of everyday spending, especially as prices for essentials fluctuate.

Together, these patterns illustrate a financial landscape where traditional long-term debt and newer, behavior-driven borrowing coexist.

Financial Experiences Differ Across Desk and Deskless Workers

The survey also shows that financial stress does not show up the same way for all types of workers. Desk and deskless employees share many of the same long-term habits, including high rates of retirement saving, but their day-to-day financial pressures look different.

Deskless workers are more likely to carry personal debt (88%, compared to 69% of desk workers), and they report higher levels of health impacts related to financial stress. Mental-health effects were more common among deskless employees (54% vs. 46%), as was sleep disruption (50% vs. 38%). These differences suggest that the experience of financial stress is shaped not only by financial behavior, but by the structure and predictability of work.

In a year defined by rising costs and ongoing uncertainty, these patterns highlight how financial stress is influenced by both economic conditions and the realities of people’s working lives.

Rethinking Financial Wellness at Work

Taken together, the survey results point to a broader conclusion. Financial wellness today is not defined solely by income, benefits, or savings rates. It’s defined by clarity, confidence, and the ability to make informed decisions in the face of complexity.

For employers, this represents an opportunity. As financial stress increasingly affects health, focus, and engagement, providing employees access to personalized financial guidance can meaningfully improve outcomes for individuals and organizations alike.

At Addition Wealth, we believe financial expertise should be accessible, practical, and responsive to real life, helping people not only improve their finances, but feel more confident navigating them.

Individuals with access to personalized guidance from Addition Wealth reported positive impact including:

77% of users report moderate to high financial health, compared to 64% of non-users

Only 51% of users report health impacts related to financial stress, versus 64% of non-users

66% of users engage with their finances daily, reflecting proactive management rather than avoidance

About the Survey

Addition Wealth’s 2025 Employer Survey included respondents across a range of industries, income levels, and roles, reflecting the experiences of a modern workforce navigating financial complexity.

Sources:

¹–⁷Addition Wealth, 2025 Employee Survey (New York: Addition Wealth, 2026).

New findings from Addition Wealth show how rising costs and economic volatility affected employees across income levels.

Key Survey Findings at a Glance

58% of employees report moderate to high stress, including half of those who say they are in a strong financial position

71% of employees would feel moderate to high stress if their paycheck were delayed by just one week

57% of employees report health effects from financial stress, and among those highly stressed, 86% experience at least one health impact¹

In many ways, 2025 was expected to be a year of financial stabilization. Inflation cooled from 2022 peaks and many households continued saving and planning for the future. Yet for many individuals, financial stress didn’t ease this year, it intensified.

Rising everyday costs, new tariffs affecting the price of goods, and continued economic uncertainty reshaped how people experienced their finances this year. Trade policy changes increased costs across supply chains, showing up in the prices of everyday essentials. We saw some highly visible price spikes, such as the cost of eggs and coffee reaching record highs.

Against this backdrop, Addition Wealth conducted its 2025 Employee Survey to better understand how employees were navigating their finances. The findings reveal an important shift: financial stress in 2025 was less about income or savings alone, and more about uncertainty, confidence, and the ability to manage change. Across industries, roles, and income levels, people are doing many of the “right” things financially, yet stress persists.

People are saving, planning, and staying engaged

Across respondents, most people are taking consistent steps to manage their finances, even amid uncertainty. Saving for retirement also emerged as the top goal overall, with 61% listing it as a priority.²

Respondents identified a range of financial goals for the year, reflecting both long-term planning and day-to-day financial needs.³

61% are saving for retirement

49% are paying off debt

38% are investing

31% are building an emergency fund

29% are saving for a home

28% are budgeting and managing day-to-day spending

18% are managing unexpected expenses

Taken together, these goals show a workforce that is actively trying to build stability in a year marked by uncertainty. People are saving, planning, and prioritizing what they can control, even as broader economic conditions continue to shape how confident they feel day to day.

Stress Persists Even When Finances Are Strong, Impacts Health, Relationships, and Work

More than half of survey respondents (58%) reported moderate to high financial stress and that stress does not disappear with stronger financial health. Even among individuals who rated their finances as strong, 50% still reported moderate to high stress, and 31% experienced health impacts related to financial pressure.⁴

These findings point to an important shift. Financial wellbeing today is no longer defined solely by income, savings, or benefits. It is increasingly shaped by confidence, clarity, and the ability to manage ongoing change. Without guidance and structure, even financially stable individuals can feel overwhelmed by money.

The effects of financial stress extend well beyond finances. Across respondents:

57% reported health impacts, most commonly affecting mental health (49%) and sleep (39%)

29% said financial stress strained their relationships

37% reported difficulty focusing at work⁵

Among individuals experiencing high financial stress, the impact is even more pronounced: 86% reported at least one health-related effect, underscoring how deeply financial pressure influences overall wellbeing and daily functioning.

Younger Generations Are Engaged and Under Pressure

Millennials and Gen Z reported the highest levels of financial stress, with 88% experiencing moderate to high stress. At the same time, they are highly engaged:

93% think about their finances daily or weekly

Retirement savings, emergency funds, and debt repayment are top priorities⁶

Our survey found that 76% of employees have debt, yet only 39% actively follow a debt plan, compared to 48% of Baby Boomers.⁷ This combination of high awareness and low follow-through suggests that engagement alone isn’t enough. Without clear frameworks and guidance, constant attention to finances can increase stress rather than reduce it.

The Mix of Debt Is Changing, Adding New Layers to Financial Stress

Debt continues to be a reality for many households, but the types of debt people carry in 2025 show how financial pressures have evolved. More than half of respondents (52%) hold credit card debt, and many also manage auto loans (39%), student loans (27%), personal loans (19%), or medical debt (13%).

A notable shift is the growing presence of short-term installment debt. Ten percent of respondents report Buy Now, Pay Later (BNPL) balances, reflecting how these tools have become part of everyday spending, especially as prices for essentials fluctuate.

Together, these patterns illustrate a financial landscape where traditional long-term debt and newer, behavior-driven borrowing coexist.

Financial Experiences Differ Across Desk and Deskless Workers

The survey also shows that financial stress does not show up the same way for all types of workers. Desk and deskless employees share many of the same long-term habits, including high rates of retirement saving, but their day-to-day financial pressures look different.

Deskless workers are more likely to carry personal debt (88%, compared to 69% of desk workers), and they report higher levels of health impacts related to financial stress. Mental-health effects were more common among deskless employees (54% vs. 46%), as was sleep disruption (50% vs. 38%). These differences suggest that the experience of financial stress is shaped not only by financial behavior, but by the structure and predictability of work.

In a year defined by rising costs and ongoing uncertainty, these patterns highlight how financial stress is influenced by both economic conditions and the realities of people’s working lives.

Rethinking Financial Wellness at Work

Taken together, the survey results point to a broader conclusion. Financial wellness today is not defined solely by income, benefits, or savings rates. It’s defined by clarity, confidence, and the ability to make informed decisions in the face of complexity.

For employers, this represents an opportunity. As financial stress increasingly affects health, focus, and engagement, providing employees access to personalized financial guidance can meaningfully improve outcomes for individuals and organizations alike.

At Addition Wealth, we believe financial expertise should be accessible, practical, and responsive to real life, helping people not only improve their finances, but feel more confident navigating them.

Individuals with access to personalized guidance from Addition Wealth reported positive impact including:

77% of users report moderate to high financial health, compared to 64% of non-users

Only 51% of users report health impacts related to financial stress, versus 64% of non-users

66% of users engage with their finances daily, reflecting proactive management rather than avoidance

About the Survey

Addition Wealth’s 2025 Employer Survey included respondents across a range of industries, income levels, and roles, reflecting the experiences of a modern workforce navigating financial complexity.

Sources:

¹–⁷Addition Wealth, 2025 Employee Survey (New York: Addition Wealth, 2026).